As discussed in past posts, there are many different scoring models, resulting in different credit scores. When applying for a mortgage, people often like to know up front what their credit score is, in order to have an idea of what loan type and what loan amount they will be eligible for. Many companies claim to be selling your real credit score to you.

Though it is a real credit score, it does not necessarily mean that it is the scoring model that mortgage banks will use when applying for a mortgage. The question is, which credit score model do mortgage banks use?

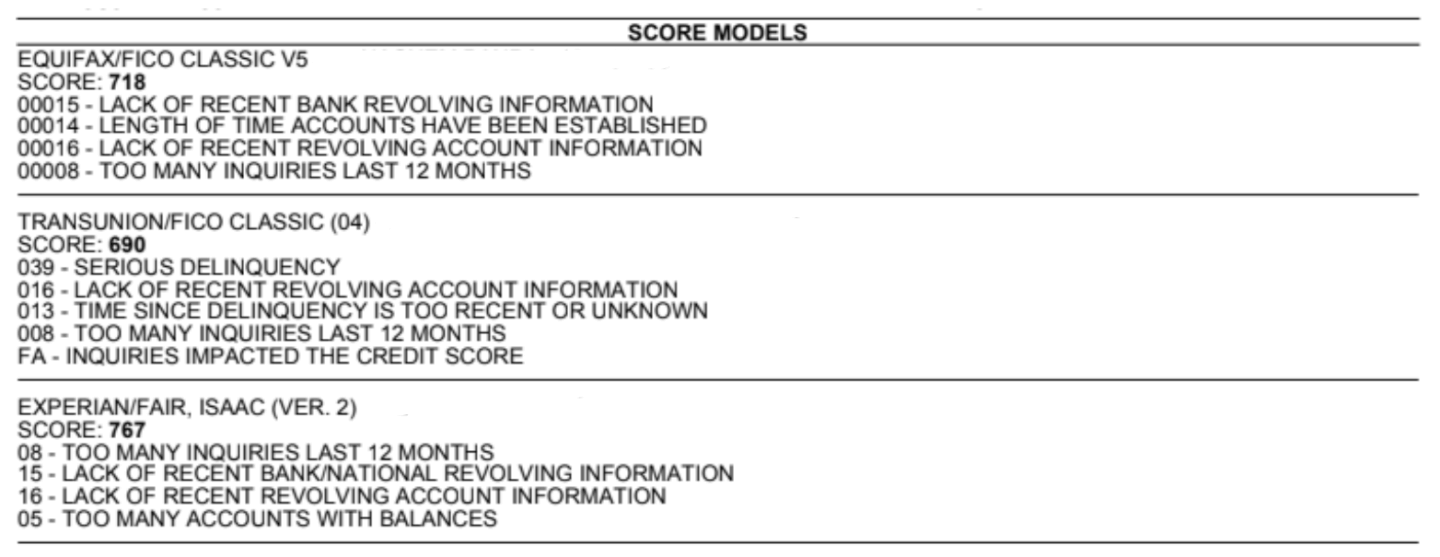

Scoring model used for mortgages

Just like Apple releases an improved iPhone every so often, so does FICO release improved scoring models every so often. But because mortgage loans are regulated by the government, it takes them very long to adapt to the newer scoring models. Mortgage loans currently still use old Fico scoring models.

When applying for a mortgage, your credit score based on your Experian credit report will be the FICO 02 score which is the second generation score from FIC0.

Your credit score based on your Transunion credit report will be your FIC0 04 and your credit score based on your Equifax credit report will be your FICO Beacon 5 score (also known as FICO V5 score).

Both the FICO 04 and the Beacon 5 are the same generation score (Equifax calls it Beacon 05 because when Fico started out in 1993 they were only building scores for Equifax. Therefore, Equifax has more generations of Fico scores than the other credit bureaus).

Which score will be used of the three credit bureaus?

The final score your mortgage will be based on will be the middle of the three scores.

Many people think it’s the average score between the Equifax, Transunion, and Experian scores, but it’s not. The score that‘ll be used for the mortgage is the actual middle score. Not the highest one and not the lowest one, but the middle one. So if your Transunion score is 725, Experian score 756, and Equifax score is 689, the score the mortgage bank will use is your Transunion one, at 725 since it is the number in between the other two.

Where can I view my mortgage credit scores?

Here are the websites where you can buy and view your mortgage credit scores.

MYFico

MYFico gives you multiple credit scores including your FICO Mortgage Lending score. You can view all your scores for all three credit bureaus.

- Price: There are three package options.

Basic: Only Experian is updated every month- $19.95

Advanced: All three credit bureaus are updated every 3 months- $29.95

Premier: All three credit reports are updated every month- $39.95 - Updated: This depends on the plan.

- Accuracy: MyFico is the most accurate place to get your FICO score.

Experian

Experian gives you multiple credit scores including your mortgage credit score. You can only view your mortgage score from Experian and not from the other two credit bureaus.

- Price: Free 7-day trial, then $24.99 per month

- Updated: Experian scores- every day. Transunion and Equifax- once in 30 days

- Accuracy: In my experience, the scores are pretty close to the real scores.

Extra Credit

Extra Credit gives you multiple credit scores including your mortgage credit score. You can view your mortgage score from Experian, TransUnion, and Equifax.

- Price: Free 7-day trial, then $24.99 per month

- Updated: Every 30 days

- Accuracy: The first score on the list under mortgage score is the one that is most widely used (Experian Fico 02, Equifax Beacon 05, Transunion Fico 04). The scores are pretty close to the real scores.

Thank you for this very helpful info!

ExtraCredit seems to only be a 7 day trial though.

Thanks. I will update the post accordingly