There is a famous joke about a guy who won the lottery. When asked what he would do with the money, he said he would use the money to pay off his debt. When asked what he would do with the rest, he answered, “The rest will have to wait until the next time I win the lottery.”

If you ever find yourself with extra cash (or if you win the lottery), at times, you will have enough to pay part of your credit card debt, but not all.

This takes us to today’s post. Which credit card should you pay first in order to get your score improved even if you can’t pay up all your credit card debt?

This post will be full of calculations, so make sure you have a calculator handy.

The credit utilization brackets

Fico categorizes credit utilization based on brackets which are believed to be the following (please note, the real Fico brackets are confidential info which is not publicly available. The brackets shown below are just an educated guess).

Bracket #1 [0%-9%]

Bracket #2 [9.1%-29%]

Bracket #3 [29.1%-49%]

Bracket #4 [49.1%-79%]

Bracket #5 [79.1%-100%]

Bracket #6 [100% plus]

0% shows no money has been used on the card. Balance is at zero.

100% shows the full credit limit amount has been used on the card. 100% plus would be a card on which the balance is higher than the credit limit.

Please make sure you understand the brackets as you will need to remember this information going further in the post.

Credit utilization only affects personal credit cards – most business credit cards do not get reported on your personal credit report. So, don’t worry about them affecting your credit. (Exceptions would be most Capital One business cards (except for the Capital One Spark Plus card), Discover business cards, and some other smaller credit card issuers, which report business cards on personal credit reports).

Calculate your credit utilization

Knowing the credit utilization percentage on each card will help you pay up your balances efficiently. Credit utilization is the percent of your credit limit you actually used.

Every one of your credit cards has a credit limit which is the maximum amount of money you are allowed to spend with that card. Then there is the balance which is the amount of money you spent on your card.

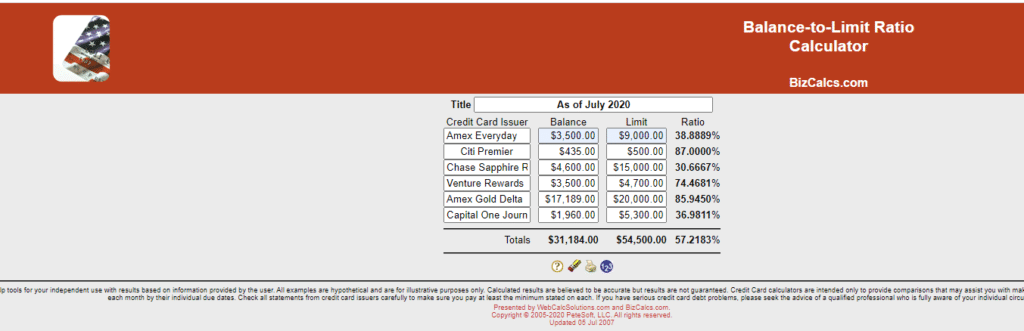

See the sample chart below with the credit card name, credit limit, and balance listed. Make your own chart by filling in the credit cards, credit limits, and balances, along with how much money you have available to make some payments.

| Credit Limit | Balance | Utilization | Difference (%) Needed To Pay To Get To 29% | Difference ($) Needed To Pay To Get To 29% | |

| Amex Everyday | $9,000 | $3,500 | 38.89% | ||

| Citi Premier | $500 | $435 | 87.00% | ||

| Citi Custom Cash | $15,000 | $4,600 | 30.67% | ||

| Venture Rewards | $4,700 | $3,500 | 74.47% | ||

| Amex Gold Delta | $20,000 | $17,189 | 85.95% | ||

| Capital One Journey | $5,300 | $1,960 | 36.98% | ||

| Wells Fargo Propel | $1,200 | $200 | 16.67% | ||

| Amazon Card | $4,000 | $1,300 | 32.50% | ||

| Costco Anywhere | $2,250 | $776 | 34.49% | ||

| Available Money | $3500 |

To calculate credit utilization, divide the balance by the credit limit then multiply the result by 100. You now end up with a percentage which is your credit utilization.

Try out this calculator to plug in your numbers and get your results.

Balance-to-Limit Ratio Calculator

Make sure to prepare a chart

Unless you’re a math genius, you’re not going to remember everything we discussed in this post by heart. Prepare an excel sheet for yourself, similar to the one we posted above. Plug in your cards and numbers and then continue reading the post.

Here’s a sample chart.

Learn the goal of paying off your balances

The goal of paying off your credit card balances is to get as many as possible into the 2nd credit utilization bracket, a max of 29%. That is considered rational credit utilization. 29.1% is already considered part of the next bracket, which is much worse. Scoring models do not look at the amount of the balance, rather they look at the credit utilization number. They like to see you keep a lot below your credit limit.

Turns out, you don’t even have to pay up the full amount. You could pay up the card with as much money it takes to get it to 29%.

Let’s break up this concept using our sample chart.

Example 1:

Amex Gold Delta has a high balance of $17,189.

| Credit Limit | Balance | Utilization | Difference (%) Needed To Pay To Get To 29% | Difference ($) Needed To Pay To Get To 29% | |

| Amex Gold Delta | $20,000 | $17,189 | 85.95% |

The instinct reaction would be to knock off that balance first. But hold it. Whatever money you have on hand might not cover the full balance. Even if it does, you still would need money left over for the rest of the balances.

Take this a step further. The credit utilization on the Amex Gold Delta is 85.95%. I mentioned above that we want to get as many credit utilization numbers down to 29%. You would need lots of money to get the balance to 29% credit utilization.

Example 2:

On the other hand, the Wells Fargo Propel has a relatively low balance of $200.

| Credit Limit | Balance | Utilization | Difference (%) Needed To Pay To Get To 29% | Difference ($) Needed To Pay To Get To 29% | |

| Wells Fargo Propel | $1,200 | $200 | 16.67% |

Pay that off, easy, and done with? No, doing that will not improve your score much. It is already in a good credit utilization bracket, with a number of 16.67%. You would leave that balance for now.

Example 3:

The Citi Custom Cash has a balance of $4,600. That might be out of your budget right now. Credit utilization is 30.67% which is so close to 29%, our goal number. Meaning, to get this card to have a good credit utilization number, all you would pay is 1.67% of the balance. That equals just $76.82. Fair enough?

| Credit Limit | Balance | Utilization | Difference (%) Needed To Pay To Get To 29% | Difference ($) Needed To Pay To Get To 29% | |

| Citi Custom Cash | $15,000 | $4,600 | 30.67% |

Calculate how much of the credit card balance to pay

Here is how to calculate how much of the balance you need to pay to get it to 29%.

First figure out the amount in dollars your balance should be to have a credit utilization below 29%. Take the credit limit and divide it by 100. Multiply the result by 29. The result in dollars is what your balance should be after paying.

To figure out how much of your balance to pay to get to that amount, subtract the amount from your balance. That is how much you should pay so that your balance results in a credit utilization of 29%

Now you can refer back to your chart and make a list of how much you would need to pay for each card to get to 29% credit utilization.

Tackle the balances

According to your budget, start with the cards which are closest to 29%. You will pay off the difference needed to get the balance to the below 29% bracket. Do so until you use up the available money you have to pay up the balances.

Distribute the extra money over larger balances

If you can’t get all cards below 29%, or if you find yourself with extra money, aim to get the rest of the cards within the 29.1%-49% bracket. Still left over with balances not in that range, aim next for the 49.1%-79% bracket, and so forth.

Let’s see how we would work that out with our sample chart.

| Credit Limit | Balance | Utilization | Difference (%) Needed To Pay To Get To 29% | Difference ($) Needed To Pay To Get To 29% | |

| Amex Everyday | $9,000 | $3,500 | 38.89% | 9.89% | $890 |

| Citi Premier | $500 | $435 | 87.00% | 58% | $290 |

| Citi Custom Cash | $15,000 | $4,600 | 30.67% | 1.67% | $250 |

| Venture Rewards | $4,700 | $3,500 | 74.47% | 45.47% | $2,137 |

| Amex Gold Delta | $20,000 | $17,189 | 85.95% | 56.95% | $11,389 |

| Capital One Journey | $5,300 | $1,960 | 36.98% | 7.98% | $423 |

| Wells Fargo Propel | $1,200 | $200 | 16.67% | – | – |

| Amazon Card | $4,000 | $1,300 | 32.50% | 3.50% | $140 |

| Costco Anywhere | $2,250 | $776 | 34.49% | 5.49% | $123.50 |

| Available Money | $3500 |

- I would start with the following cards: Amex Everyday, Citi Premier, Citi Custom Cash, Capital One Journey, Amazon Card, Costco Anywhere. Those all have the smallest amount to pay (according to the % difference) to get to a credit utilization of 29%.

- That totals $2,116.50 out of $3500 available. I have 2 credit card balances left after that, Venture Rewards and Amex Gold Delta. I want to get those into the 49% bracket at least and I have $1,383.50 to work with.

- The Venture Rewards card needs $1197 paid to get to 49%. I will pay that much up.

- The Amex Delta Gold card needs $7389 paid to reach 49%. Too much for now. It needs $4200 to reach 79%. I can’t pay that either. Maybe soon when I have more money.

Follow these steps and watch your credit card balances drop and your credit score soar:)

Please Note: Different credit cards have different interest rates. This post is a strategy on how to increase your credit score by the most points with paying the least balances. This is not a post on how to save the most on interest. You can learn how to pay your balances to save on interest here.

The amount of helpful, informative and easy to understand information on this website is second to none.

i allways new that the credit is based on your overall balance, and not by every card, so for example if i would have a card with a $500 credit limit maxet out, but i also have a differnet card with a $20,000 credit limit, which has a 0 balnce, than my score wouldnt be affected. was i mistaking?

That’s a common mistake. Utilization is counted each card separately.

i think that both are rite, it depends on both. [that was my answer after googling it]