You’ve seen it all over, but you may (or may not) have been embarrassed to ask what it means. (And you may (or may not) have googled the term but you still don’t quite get it.)

In this post, we’ll discuss the simple meaning of 0% APR so that you actually get what it means and see how you can benefit from it.

Spill the beans- what does 0% APR mean?

If you’re above the age of two, you know what 0 means. And if you’re above the age of 10, you know what % means. So the 0% is not the difficult part.

APR stands for Annual Percentage Rate, which means the interest rate that you pay on your credit card bill.

If a person pays 24.99% interest on their credit card, then their credit card APR is 24.99%.

You can obviously deduce from that that if a person’s credit card APR is 0% then they pay 0% interest.

Hold it. How is that possible?

You’d think these credit card companies are smarter than that. Why would they offer 0% APR? What’s the catch?

The answer is that there is no catch. When a person gets an introductory 0% APR promo, they really don’t pay interest until the promo expires.

Why do the banks offer it?

The answer is a simple one. The way banks make money (lots and lots of it) is by charging interest. A great way to catch a fish (i.e. a customer) is by offering a 0% APR promo.

The idea is to get the people to spend freely and to rack up a bill.

While you’re spending all that money (knowing you have no interest rate) the bank is murmuring prayers. They hope that you won’t be able to pay up the balance when the offer expires and at that point, they’ll start raking it in (from the interest rates applied to your extremely high bill).

Is there a way for me to avoid being the bank’s fish?

Yes! As a matter of fact, they can become yours!

If you’re like me, then a 0% APR offer is an opportunity to bank on the bank. I have successfully borrowed over $100K while paying $0 in interest. I use these loans for business expenses and sometimes even personal expenses.

I’ve also already advised many consumers and businesses on how to have the same success. They all walked out with thousands of dollars of interest-free loans. It’s even possible to get cash with 0% APR offers, by following the strategies disused here.

But in order for you to use the bank as your fish instead of being theirs, you need to make sure you’re borrowing money with a plan.

You need to have a plan of how you will pay the money once the 0% promo is up. (You can also swap the balances to new 0% APR cards once the promo expires. More details here).

Where can I find these 0% APR offers?

We have a very comprehensive list on this website of cards with 0% APR offers. This list is constantly updated with all new offers. You can check out the full list here.

What’s the difference between 0% APR on purchases and balance transfers?

Some cards offer 0% APR on purchases, some offer 0% APR on balance transfers, and some offer 0% APR on both purchases and balance transfers.

Purchases are items you buy and use the card to pay.

Balance transfers are balances that you carry with another credit card that you would like to transfer to the new card in order to get the 0% APR.

Depending on your goals you need to make sure that the card you choose offers 0% APR on the proper type of transactions. For example, if you are planning to transfer an existing balance from another credit card to the new card, then make sure to apply for a card that offers 0% APR on balance transfers.

You can read more about balance transfer here.

What else do I need to know?

Here are some additional things to know before you jump into a 0% APR offer.

Penalty APR: This is the increased interest you’ll be paying if you make a late payment. If you end up paying late, not only will you lose the 0% APR offers but you will pay an even higher interest rate- if your card has a penalty APR. (Not all cards have a penalty APR.)

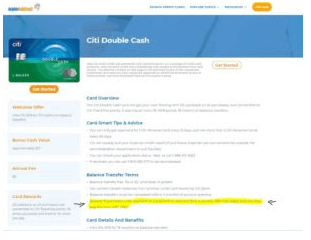

Luckily for you, we actually list by every card if it has a penalty APR or not (thank us later:) Reference to the picture to see where to find it.

Grace Period: Every card (even those without 0% APR promos) has a grace period which lasts from the day you purchase something (with your card) until the payment due date. In that time, the bank is being “nice” to you and not charging you interest on purchases. But, this is only if you pay the balance in full for that month. If you don’t pay in full, you will lose your grace period, which will lead to interest being charged (on purchases) from the day of purchase every single month until the balance is paid in full. (It will take another billing cycle after your balance is paid for the grace period to reset) .

The reason why you need to know this is because some 0% APR cards only remove the interest on balance transfers but they do charge interest on purchases (remember the difference we discussed above?) . In such a case, because you’re carrying the balance that you transferred and now have 0% APR, you lost the grace period and you will be paying interest on purchases from the day of purchase. So if your card has 0% APR on balance transfers, be careful to avoid using it to make any purchases, as you will start accumulating interest right away from the day of purchase.

You can read more about credit card grace periods here

You can’t transfer a balance from the same bank: Banks do not allow you to transfer balances from one card to another card that is issued by their bank. For example, you can’t transfer a balance from one Chase credit card to another Chase credit card. (Please note: If the bank offers you balance transfer checks or a direct deposit, then you can just deposit the check in your own bank account and then use the funds to pay back any credit card you want).

Balance transfer fee: Banks will usually charge a one-time fee to make a balance transfer. The balance transfer fee is usually approximately 3%.

I hope this post clears up any questions or confusion you may have had about 0% APR offers!

![Best Credit Cards With Airport Lounge Access [2024]](https://helpmebuildcredit.com/wp-content/uploads/2022/06/post-on-cards-with-airport-lounges.png)

![The 10 Best 0% APR Credit Cards For April [2024]](https://helpmebuildcredit.com/wp-content/uploads/2023/07/Post-on-best-0-apr-cards3-1080x675.png)

![The 10 Best Credit Card Offers For April [2024]](https://helpmebuildcredit.com/wp-content/uploads/2024/03/post-on-best-offers-april-2024.png)

0 Comments